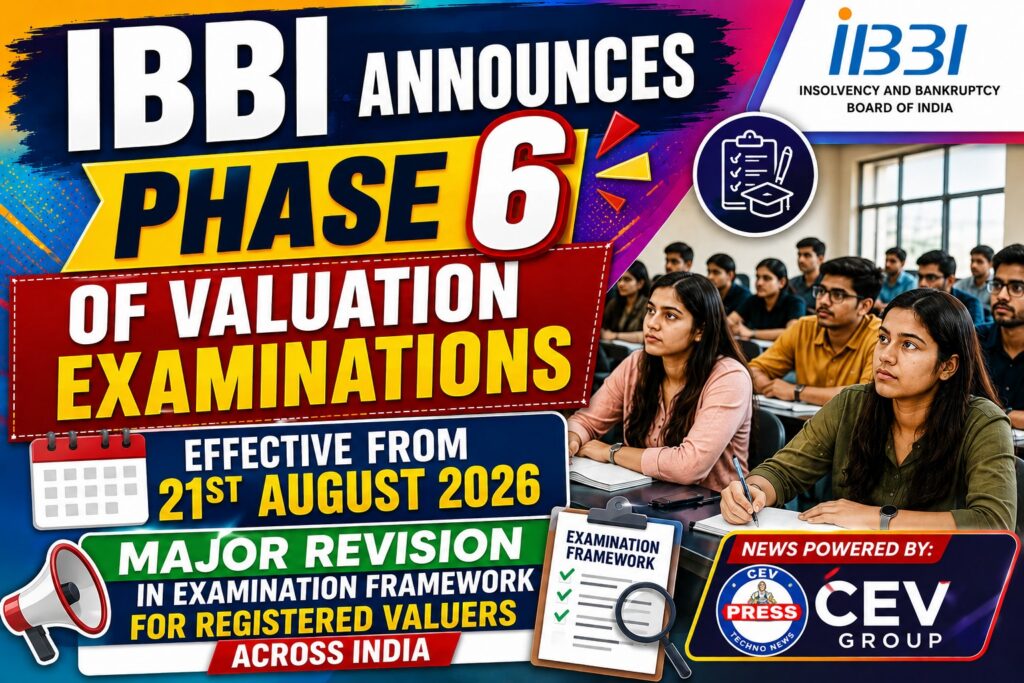

IBBI ANNOUNCES PHASE 6 OF VALUATION EXAMINATIONS EFFECTIVE FROM 21ST AUGUST 2026

Major Revision in Examination Framework for Registered Valuers Across India

NEW DELHI-21/05/2026: In a significant development for the valuation profession in India, the Insolvency and Bankruptcy Board of India (IBBI) has officially announced the commencement of Phase 6 of Valuation Examinations with effect from 21st August 2026. The announcement was made through Press Release No. IBBI/PR/2026/09 dated 20th May 2026, issued under the provisions of Rule 5(3) of the Companies (Registered Valuers and Valuation) Rules, 2017.

The move is being viewed as a landmark step towards strengthening the competency, transparency, and professional standards of Registered Valuers in India. The revised examination structure and updated syllabus are expected to have a far-reaching impact on aspiring valuers, valuation professionals, Registered Valuer Organisations (RVOs), training institutions, banks, financial institutions, insolvency professionals, and the real estate and corporate sectors at large.

According to the notification, the revised “Valuation Examinations” shall apply to all three major asset classes, namely:

- Land and Building

- Plant and Machinery

- Securities or Financial Assets

The detailed syllabus and examination format for each asset class have been published separately as Annexures I, II, and III respectively.

The examinations are conducted as part of the regulatory framework established under the Companies (Registered Valuers and Valuation) Rules, 2017, wherein the IBBI functions as the designated “Authority” for regulating the profession of Registered Valuers in India.

Importance of the Announcement

The valuation profession has gained enormous significance in recent years due to increasing reliance on professional valuation in areas such as:

- Insolvency and Bankruptcy proceedings

- Corporate mergers and acquisitions

- Financial reporting and auditing

- Banking and secured lending

- Taxation matters

- Insurance assessments

- Real estate and infrastructure projects

- Corporate restructuring and liquidation processes

With growing complexities in valuation assignments and evolving international valuation standards, the IBBI’s initiative to upgrade the examination framework is being considered a timely and necessary reform.

Experts believe that Phase 6 examinations may incorporate deeper analytical understanding, enhanced case-study-based learning, updated laws, practical valuation methodologies, ethical standards, and greater alignment with international valuation practices.

Focus on Professional Competency

The revised examination pattern is expected to place stronger emphasis on:

- Practical application of valuation principles

- Legal and regulatory compliance

- Professional ethics and conduct

- Case-study-oriented problem solving

- Financial and technical interpretation

- Market-based valuation approaches

- Contemporary valuation standards and reporting

Industry observers have noted that the new examination phase could significantly elevate the quality and credibility of Registered Valuers in India.

Impact on Students and Valuation Aspirants

Thousands of engineering professionals, architects, chartered accountants, company secretaries, cost accountants, bankers, finance professionals, and technical experts who aspire to become Registered Valuers are likely to be directly impacted by this revised framework.

Training institutions and Registered Valuer Organisations across the country are expected to update their educational material, mock tests, MCQ banks, classroom sessions, and practical training modules in line with the new syllabus.

Candidates preparing for the IBBI Valuation Examinations are advised to carefully study the revised syllabus and examination pattern before appearing in examinations scheduled from 21st August 2026 onwards.

Growing Importance of Registered Valuers

Since the implementation of the Insolvency and Bankruptcy Code and related valuation regulations, the role of Registered Valuers has become increasingly crucial in maintaining financial discipline, transparency, and fair market assessment mechanisms.

Professional valuers today play a pivotal role in:

- Determining liquidation values

- Assessing fair value of assets

- Supporting lenders and financial institutions

- Assisting courts and tribunals

- Facilitating insolvency resolution processes

- Supporting corporate governance and financial disclosures

The latest announcement by the IBBI further reinforces the government’s intent to strengthen institutional professionalism and ensure higher standards in valuation practices across India.

The 2026 syllabus is not a complete overhaul, but there are several important strategic changes that indicate IBBI is moving toward:

- more practical insolvency valuation,

- greater regulatory compliance,

- stronger data/privacy awareness,

- international valuation standards,

- more case-law based questions,

- and more professional responsibility of valuers.

Below is the detailed comparison.

Major Changes Introduced in 2026 Syllabus

- Weightage of “Laws – General” Reduced from 9% to 7%

2024:

“Laws – General” carried 9% weightage.

2026:

Reduced to 7%.

Impact

This is important because:

- direct legal theory questions may slightly reduce,

- Practical valuation and professional standards are getting more importance, and

- exam focus is shifting from pure legal theory to applied valuation practice.

However, laws are still extremely important because many valuation questions are law-based indirectly.

- BIG CHANGE – IBC Coverage Expanded

2024:

Only:

“Salient features of the Insolvency and Bankruptcy Code, 2016 concerning valuation”

2026:

Replaced with:

“The Insolvency and Bankruptcy Code, 2016 (IBC) and Regulations made thereunder.”

Why This Is Very Important

This is one of the biggest changes.

Earlier:

- Only basic valuation-related IBC concepts were needed.

Now:

- regulations are expressly included,The

- practical CIRP/liquidation valuation process becomes important,

- likely focus on:

- Fair Value,

- Liquidation Value,

- Regulation 27,

- RP appointment of valuers,

- valuation timelines,

- confidentiality,

- role of registered valuers,

- valuation methodology under IBC,

- liquidation regulations.

Practical Effect

Expect more questions on:

- CIRP valuation procedure,

- role of two valuers,

- average valuation,

- valuation confidentiality,

- valuation report handling,

- liquidation vs fair value,

- IBBI circulars and guidelines.

This is a major upgrade toward practical insolvency valuation.

- NEW TOPIC ADDED – Digital Personal Data Protection Act, 2023

Added in 2026 under Ethics:

“Digital Personal Data Protection Act, 2023 and rules made thereunder”

This Was NOT Present in 2024

Why Important

This is a completely new statutory area.

IBBI now expects valuers to understand:

- confidentiality of client information,

- handling of financial/property data,

- digital storage responsibility,

- privacy obligations,

- sharing of valuation reports,

- misuse of personal/business data.

Likely Questions

- confidentiality obligations,

- data fiduciary concepts,

- consent,

- handling borrower/corporate debtor data,

- professional misconduct involving data leakage.

This reflects modern compliance expectations.

- “Various Purposes of Valuation” Weightage Increased from 3% to 5%

2024:

3% weightage.

2026:

5% weightage.

This Is a Very Significant Strategic Change

This means IBBI wants:

- more practical valuation application,

- real-world report preparation,

- insolvency valuation procedures,

- standards and reporting compliance.

This section became much more important for scoring.

- NEW IBBI Guidelines Added

Added in 2026:

“Guidelines issued by the IBBI for Conducting Valuation under the Insolvency and Bankruptcy Code, 2016…”

Including:

- documentation,

- valuation report contents,

- receivable valuation,

- asset-specific formats,

- coordinating the valuer role,

- fair value determination.

Why Extremely Important

This is probably the most exam-relevant addition.

Questions may now come directly from:

- IBBI valuation guidelines,

- practical reporting formats,

- valuation documentation,

- role/responsibility of the coordinating valuer,

- valuation assumptions and disclosures.

This indicates:

IBBI is making the exam more practice-oriented rather than purely academic.

- NEW INTERNATIONAL VALUATION STANDARDS (IVS) Added

2026 Newly Added:

“The latest International Valuation Standards (IVS), as updated in January 2025 by the IVSC.”

2024:

No IVS reference existed.

Why This Is a Massive Change

This is one of the most important additions.

Now candidates must study:

- IVS framework,

- IVS definitions,

- bases of value,

- valuation approaches,

- scope of work,

- investigations,

- compliance,

- reporting standards.

Likely Exam Focus

- difference between IVS and Indian standards,

- market value definition,

- highest and best use,

- valuation reporting,

- ethics,

- IVS terminology.

This internationalises the exam significantly.

- Rule 11UA of the Income Tax Act Removed

2024 Included:

“as per rule 11UA of the Income Tax Act, 1961”

2026:

This specific reference is removed.

Meaning

Direct emphasis on Rule 11UA valuation may be reduced.

However:

- valuation under Income Tax may still be asked generally,

- But detailed Rule 11UA calculations may reduce in importance.

- BIG EXPANSION OF CASE LAWS

2024:

Only 10 important cases.

2026:

Five major new cases added.

Newly Added Cases

- Mano Alex v. NHAI

- Lal Chand v. Union of India

- Mehrawal Khewaji Trust v. State of Punjab

- Special Land Acquisition Officer v. Karigowda

- Bharat Kumar v. State of Haryana

Why Important

This strongly indicates:

- more land acquisition compensation questions,

- more judicial principles of valuation,

- more Supreme Court-based practical valuation principles.

Most Important Area

Land acquisition compensation jurisprudence.

Expect questions on:

- comparable sales,

- highest bona fide exemplar,

- deduction for development,

- compensation enhancement,

- market value determination.

This is a major trend change.

- Updated Law Cut-Off Date

2024:

Applicable law updates till:

31 December 2023

2026:

Updated to:

30 June 2026

Practical Effect

Candidates must now study:

- latest amendments,

- latest IBBI circulars,

- updated regulations,

- latest valuation standards.

- Examination Pattern – NO Major Change

The following remain the same in 2026:

- Online MCQ format,

- 2 hours duration,

- 60% passing,

- 25% negative marking,

- ₹5900 fee,

- calculator restrictions,

- every working day exam availability.

So: The syllabus changed more than the examination pattern.

Most Important Topics for 2026 Preparation

Based on the changes, these areas have become HIGH PRIORITY:

Highest Priority

- IBC + Regulations

- IBBI Valuation Guidelines

- International Valuation Standards (IVS)

- New case laws on land acquisition

- Practical valuation reports

- Coordinating the valuer role

- Ethics + DPDP Act

Areas Whose Importance Reduced Slightly

Reduced Relative Importance

- pure legal theory,

- Rule 11UA,

- traditional theory-only questions.

Overall Trend of 2026 Syllabus

The 2026 syllabus shows that IBBI wants valuers to become:

- practical insolvency professionals,

- internationally aligned valuation experts,

- compliance-oriented professionals,

- court-ready expert valuers,

- ethically responsible data handlers.

The exam is now clearly more:

- practice-oriented,

- standards-driven,

- professionally regulated,

- insolvency-focused.

Final TAKEAWAYS

The most important changes in the 2026 Land & Building syllabus are:

| Major Change | Importance |

| IBC + Regulations added | Very High |

| IBBI valuation guidelines added | Very High |

| International Valuation Standards (IVS) added | Very High |

| DPDP Act added | High |

| New Supreme Court valuation cases added | High |

| Practical valuation/reporting emphasis increased | High |

| Weightage of practical valuation increased | High |

| General law weightage reduced | Moderate |

| Rule 11UA removed | Moderate |

The 2026 syllabus is substantially more advanced and professional compared to the 2024 syllabus.

Chapter-wise Comparison of 2024 vs 2026 IBBI Land & Building Valuation Syllabus

| Sl. No. | Chapter / Subject | 2024 Weightage | 2026 Weightage | Change in 2026 Syllabus | Important Remarks |

| 1 | Principles of Economics – Micro & Macro Economics | 3% | 3% | No Change | Syllabus substantially same |

| 2 | Book-keeping and Accountancy | 3% | 3% | No Change | No major modification |

| 3 | Laws – General | 9% | 7% | Yes – Weightage Reduced | Greater shift from pure legal theory to practical valuation |

| IBC coverage expanded | Earlier only “salient features”; now full IBC + Regulations included | ||||

| Practical insolvency valuation added indirectly | Important for CIRP, liquidation, fair value, and liquidation value | ||||

| 4 | Introduction to Statistics | 2% | 2% | No Change | Same topics continue |

| 5 | Environmental Issues in Valuation | 3% | 3% | No Change | No major additions |

| 6 | Professional / Business Ethics and Standards | 3% | 3% | Yes – New Topic Added | Digital Personal Data Protection Act, 2023 added |

| Data confidentiality emphasis increased | Important for valuation reports and client information | ||||

| 7 | Laws related to Real Estate | 7% | 7% | No Major Change | Core real estate laws remain the same |

| 8 | Valuation of Real Estate – General Concepts | 9% | 9% | No Major Structural Change | Core valuation concepts retained |

| Income Approach to Value | 7% | 7% | No Change | Same concepts continue | |

| Market Approach to Value | 7% | 7% | No Change | Same valuation methods continue | |

| Cost Approach to Value | 7% | 7% | No Change | DRC and depreciation concepts continue | |

| Various Purposes of Valuation | 3% | 5% | Major Change – Weightage Increased | Practical valuation applications now more important | |

| IBBI Valuation Guidelines Added | Documentation, report formats, coordinating valuer, etc. | ||||

| International Valuation Standards (IVS) Added | The latest IVS, updated January 2025, included | ||||

| Rule 11UA reference removed | Direct tax valuation focus slightly reduced | ||||

| 9 | Principles of Insurance and Loss Assessment | 3% | 3% | No Change | Same insurance valuation concepts |

| 10 | Report Writing | 3% | 3% | No Major Change | Reporting still highly important practically |

| 11 | Important Case Laws on Valuation | 2% | 2% | Yes – Major Expansion | Five new Supreme Court/High Court cases added |

| Land acquisition compensation jurisprudence strengthened | Comparable sales and compensation principles important | ||||

| 12 | Case Studies | 26% | 26% | No Structural Change | Still, the most important scoring section |

| Practical application emphasis increased indirectly | New standards and IBC concepts are likely to appear | ||||

| TOTAL | 100% | 100% | Pattern unchanged | Exam structure same |

Newly Added Topics in 2026 Syllabus

| Newly Added Topic | Chapter |

| IBC and Regulations made thereunder | Laws – General |

| Digital Personal Data Protection Act, 2023 | Ethics & Standards |

| IBBI Guidelines for Conducting Valuation under IBC | Various Purposes of Valuation |

| International Valuation Standards (IVS) – January 2025 | Various Purposes of Valuation |

| Role of Coordinating Valuer | Various Purposes of Valuation |

| Asset-specific Valuation Report Formats | Various Purposes of Valuation |

| Valuation of Receivables | Various Purposes of Valuation |

| Five New Landmark Case Laws | Important Case Laws |

Newly Added Important Case Laws in 2026

| Case Law Added in 2026 | Importance |

| Mano Alex v. NHAI | Land acquisition compensation |

| Lal Chand v. Union of India | Comparable sale method |

| Mehrawal Khewaji Trust v. State of Punjab | Highest bona fide exemplar principle |

| Special Land Acquisition Officer v. Karigowda | Market value determination |

| Bharat Kumar v. State of Haryana | Compensation and valuation principles |

Topics Removed / Reduced in Importance

| Topic | Status in 2026 |

| Rule 11UA of the Income Tax Act, 1961 | Specifically removed |

| Pure legal theory focus | Reduced |

| Only the “salient features” approach under IBC | Replaced with broader practical regulatory coverage |

Most Important High-Scoring Areas for 2026 Exam

| Priority | Topic |

| Very High | Case Studies (26%) |

| Very High | Valuation of Real Estate + Approaches |

| Very High | IBC Regulations and Valuation Guidelines |

| Very High | IVS (International Valuation Standards) |

| High | Practical Valuation Reports |

| High | New Case Laws |

| High | Ethics + DPDP Act |

| Moderate | General Laws |

| Moderate | Economics & Statistics |