IMPACT OF BLACK MONEY OR PARALLEL ECONOMY IN PROPERTY VALUATION

How Undisclosed Cash Transactions Distort the Real Estate Market and Challenge Professional Valuation in India

India’s real estate sector has historically been one of the largest absorbers of unaccounted money. The presence of black money—unreported income circulating outside the formal financial system—has created a parallel economy that significantly distorts property valuation, market transparency, and the integrity of financial transactions.

For Registered Valuers, financial institutions, policymakers, and homebuyers, the presence of black money in property transactions poses a serious challenge. It leads to inflated market prices, unreliable transaction data, and a persistent gap between the declared value of property and the actual transaction price.

This article examines the legal, economic, and professional implications of black money in property valuation, along with the regulatory measures adopted by the Government of India to address the issue.

Understanding Black Money and the Parallel Economy

Black money refers to income that is generated through illegal activities or through legitimate activities that are deliberately concealed from tax authorities. Such income is typically unaccounted for in official financial records and is often transacted in cash to avoid detection.

Black money may arise from several sources, including:

-

Tax evasion

-

Corruption and illegal commissions

-

Unreported business income

-

Political funding and election expenditure

-

Underground economic activities such as smuggling, narcotics, and illegal trade

Because this income remains outside the formal taxation system, it forms part of the shadow or parallel economy, operating alongside the legitimate economy but without regulatory oversight.

The real estate sector has historically been a preferred destination for such funds due to the ease of integrating cash components into property transactions.

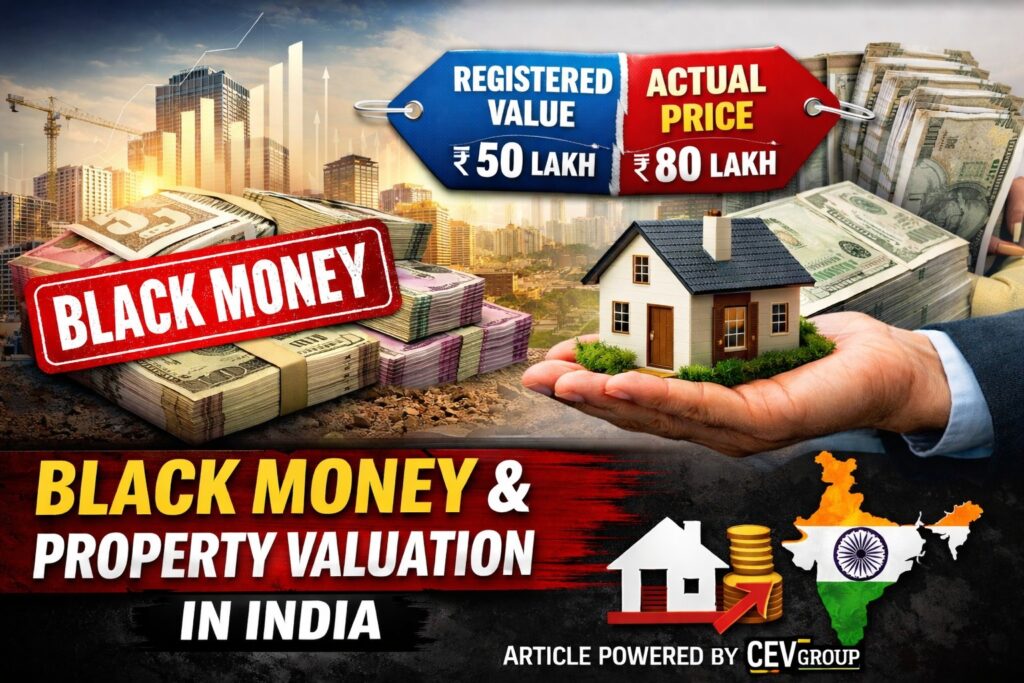

Two-Tier Pricing System in Real Estate Transactions

One of the most visible consequences of black money in the property market is the emergence of a dual pricing system.

In many property transactions:

-

The officially registered price is declared in the sale deed for stamp duty and taxation purposes.

-

The actual market price paid by the buyer may include an additional undisclosed cash component.

This system creates a significant divergence between recorded transaction values and the true market price, making reliable property valuation extremely difficult.

For example:

| Component | Nature |

|---|---|

| Registered Value | Declared for stamp duty and registration |

| Cash Component | Undisclosed payment outside the formal system |

As a result, official records often understate the actual market value of property.

Key Impacts of Black Money on Property Valuation

1. Artificially Inflated Property Prices

The inflow of large volumes of unaccounted cash into real estate often fuels speculative investments, particularly in urban land and premium residential segments.

Because investors with black money are less sensitive to price fundamentals, this demand can:

-

Drive property prices far beyond intrinsic value

-

Create speculative bubbles

-

Reduce housing affordability for middle-class buyers

In metropolitan areas, land prices may increase not because of genuine demand but due to cash-driven speculation.

2. Distorted Market Data

Property valuation depends heavily on comparable sales data. When sale transactions are underreported, the data available in official records becomes unreliable.

Consequently:

-

Comparable sale analysis becomes distorted

-

Official land registry values do not reflect the real market trend

-

Valuers struggle to determine true fair market value

This distortion directly impacts the accuracy and credibility of valuation reports.

3. Mortgage Valuation Challenges

Banks and financial institutions rely on professional valuers to determine the security value of property offered as collateral.

However, when property transactions contain large unreported cash components:

-

Comparable sales data becomes unreliable

-

Market trends become unclear

-

Loan-to-value assessments may become inaccurate

This increases the risk exposure of lending institutions and complicates credit appraisal processes.

4. Creation of Speculative Real Estate Bubbles

Black money can act as a price cushion in the property market, preventing natural market corrections.

Even when genuine demand weakens, property prices may remain artificially high due to:

-

Cash-driven investments

-

Parking of undisclosed wealth in land and property

-

Limited transparency in property ownership

Such speculative bubbles eventually destabilize the real estate sector.

Economic Consequences of Black Money

The presence of black money in the property market has broader implications for the national economy.

Loss of Government Revenue

Underreporting of property values leads to:

-

Reduced stamp duty collections

-

Lower capital gains tax revenue

-

Reduced income tax compliance

This results in significant losses to the public exchequer.

Reduced Housing Affordability

Artificially inflated property prices make housing inaccessible to many citizens.

The impact is particularly severe in urban areas where:

-

Land supply is limited

-

Demand is high

-

Speculative investment is widespread

This widens the housing affordability gap.

Increased Future Tax Liability for Buyers

Buyers who pay a significant portion of the purchase price in cash face problems during resale.

Because the recorded purchase price is lower, their capital gains tax liability increases when they sell the property.

Risky and Non-Transparent Transactions

Cash-based transactions expose both buyers and sellers to several risks:

-

Fraudulent deals

-

Lack of legal documentation

-

Limited legal recourse in disputes

In many cases, if a transaction collapses, the buyer cannot legally recover the cash component.

Legal Framework to Curb Black Money in Real Estate

The Government of India has introduced several legal provisions to reduce the use of black money in property transactions.

Section 50C of the Income Tax Act

Under Section 50C:

If the declared sale consideration is lower than the Stamp Duty Value (SDV), the SDV is deemed to be the actual sale consideration for calculating capital gains.

This provision discourages undervaluation of property transactions.

Benami Transactions (Prohibition) Act

The Benami law aims to prevent the practice of holding property in the name of another person to conceal ownership or the source of funds.

Under this legislation:

-

Benami properties can be confiscated by the government

-

Offenders may face imprisonment of up to seven years

This law targets the concealment of black money through proxy ownership.

Real Estate Regulatory Framework

The implementation of Real Estate (Regulation and Development) Act, 2016 has significantly improved transparency in the real estate sector.

RERA mandates:

-

Project registration

-

Disclosure of project details

-

Protection of homebuyers’ interests

-

Regulation of developers

These provisions have improved accountability and transparency in property transactions.

PAN–Aadhaar Monitoring of High-Value Transactions

Mandatory quoting of PAN in high-value transactions and linking financial activities with Aadhaar enables tax authorities to track suspicious financial activity.

This digital monitoring has significantly strengthened financial surveillance mechanisms.

Legal Limits on Cash in Property Transactions

Indian law places strict restrictions on cash payments in property dealings.

Advance Payments

Under Section 269SS of the Income Tax Act:

-

Advances or loans of ₹20,000 or more cannot be accepted in cash.

Cash Transaction Limits

Under Section 269ST:

-

No person can receive ₹2 lakh or more in cash from a single person in a day or for a single transaction.

Refunds

Under Section 269T:

-

Refunds exceeding ₹20,000 must be made through banking channels, not in cash.

Penalties and Legal Consequences

Violations of cash transaction rules can result in severe penalties.

Monetary Penalty

Under Sections 271D and 271DA:

-

The penalty can be equal to the entire amount received in cash.

Taxation of Unexplained Cash

Unexplained income may be taxed at rates exceeding 60%, along with surcharges and penalties.

Benami Property Confiscation

Properties purchased through undisclosed funds may be confiscated under Benami law, and offenders may face imprisonment.

Magnitude of the Shadow Economy in India

Various economic studies suggest that the shadow economy in India may constitute nearly 20% of GDP.

Additionally:

-

Estimates indicate illicit financial outflows of approximately $64 billion annually over the past decade.

-

Deposits linked to Indian entities in Swiss banks reportedly exceeded ₹31,000 crore in recent disclosures.

While not all such funds are illegal, these figures highlight the persistent issue of offshore wealth storage and capital flight.

Measures to Reduce Black Money in the Property Market

Addressing the problem requires both policy reforms and institutional vigilance.

Key measures include:

-

Simplification and rationalization of tax laws

-

Digitization of property registration systems

-

Promotion of cashless transactions

-

Strengthening anti-money laundering regulations

-

International cooperation to track illicit financial flows

-

Greater transparency in political funding

-

Public awareness on the economic harm caused by black money

-

Enhanced data analytics and financial intelligence monitoring

Role of Registered Valuers in Ensuring Market Integrity

Professional valuers play a critical role in maintaining transparency and credibility in the real estate market.

Registered valuers must:

-

Rely on verifiable market evidence

-

Maintain professional independence

-

Document valuation assumptions carefully

-

Avoid relying on undocumented cash transaction data

Accurate valuation practices contribute significantly to financial stability and ethical market functioning.

Published by: Council of Engineers and Valuers (CEV)