ENVIRONMENT AND VALUATION

ECONOMIC VALUATION OF ENVIRONMENTAL SERVICES

Presenter: Dr M K Kaushik,

Assistant Professor of Civil Engineering,

DAV Institute of Engineering and Technology (DAVIET),

Jalandhar, Punjab

INTRODUCTION

The detailed study summarizes survey methodological issues in valuing environmental resources and outlines standard techniques to monetize environmental damages or amenities, with a focus on water resources and life cycle considerations. Key valuation approaches discussed include market-based methods (market prices, shadow prices), replacement or restoration costs, hedonic pricing, travel-cost methods, and contingent valuation (CVM) for non-market values. Non-market values are further broken down into use values (direct, recreational) and nonuse values, which comprise option, bequest, and existence values; CVM is presented as a flexible tool to elicit willingness to pay for both use and nonuse benefits.

The study emphasizes the need to consider avoided damages and changes in consumer/producer surplus when evaluating environmental improvements or controls (e.g., sulfur emissions from power plants or wetland preservation). In hedonic pricing, environmental amenities are mapped onto property values, illustrating how proximity to pollution sources (like landfills or airports) can affect housing prices and how two-stage hedonic methods address variable effects by distance.

Travel-cost methods are described as a way to value recreational sites (e.g., national parks or Lumpinee Park in Bangkok) by estimating willingness to pay from travel expenses and visitation rates, highlighting data requirements and potential biases. Contingent valuation is presented with a detailed framework for designing surveys, scenario presentations, and valuation questions, including critical issues such as survey design, payment mechanisms, and mode of data collection; ethical and moral considerations are noted.

Case studies demonstrated how nonuse values (option, bequest, existence) can constitute a significant share of total value, as seen in wilderness designation valuation exercises, where doubling area does not double value – The water resources valuation section discusses Dublin Principles and Integrated Water Resources Management (IWRM) as foundations for recognizing water as an economic good, with emphasis on valuing water beyond basic needs to inform efficient and equitable allocation. Major impetuses for water valuation include informing infrastructure investment, pricing and property-rights design, and potential markets for tradable water rights, while acknowledging the limitations of using market prices alone. Major estimation techniques for water value include residual value (value of water’s marginal product), production-function approaches, and programming models, as well as hedonic pricing and opportunity-cost comparisons for different energy sources.

Life Cycle Cost Analysis (LCCA) is also introduced as a process to evaluate total costs of water supply projects over their useful life, including development, construction, operation, maintenance, rehabilitation, and end-of-life disposal; it emphasizes comparing alternatives on a uniform time basis. The LCCA framework outlines five steps (establish design alternatives, determine activity timing, estimate costs, compute life-cycle costs, analyze results) and highlights differences between economic and financial analyses, underscoring objective alignment toward the least-cost long-term solution.

The study distinguishes residual-value methods, optimization models, and asset-based approaches for water valuation, noting challenges in data requirements, aggregation to national scales, and applicability across multiple uses.

ECONOMIC VALUATION OF ENVIRONMENTAL SERVICES

Points of Discussion

- Methodological issues of imputing values to environmental resources;

- Various standard techniques to environmental damage or amenities

- Cost–benefit analysis and ethics of discounting the future

- Case studies

VALUATION OF WATER RESOURCES

Introduction

Valuation is the art of scientifically determining the price that a willing buyer would pay to a willing seller for the transfer of thing. In the context of the immovable properties, it is the estimation of that price which the prospective purchaser will pay, and the prospective seller will accept, for transfer of the immovable property. An immovable property is, in effect, a bundle of rights in a landed property. It is possible that in some cases, it may not be the intention to transfer all rights in the landed property. In that event, the valuation will mean the determination of the price of only those rights as are intended to be transferred.

Economic Valuation of Environmental Services

- Benefits from environmental improvement- assessment of avoided environmental damages.

- Ex1- clean up a lake–aesthetic value

- Ex-2-preservation of wetland area- biodiversity, flood control, enhanced environmental amenities.

- Environmental damage costs–externalities

Methodological Issues

- Measurement of benefit-Willingness to pay

- Individuals preferences Vs social benefits

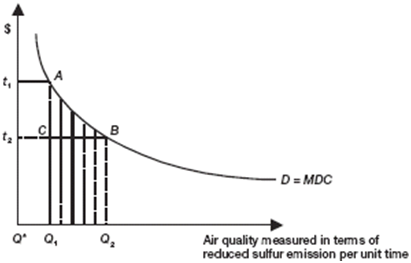

Case 1 SULFURE MISSIONS CONTROL FROM POWER PLANTS

- Benefit-improved air quality (lowering sulfur emissions).

Figure 1 Sulfure Missions Control from Power Plants (Case study related to willingness to change)

Figure 1 Sulfure Missions Control from Power Plants (Case study related to willingness to change)

- Valuation based on human preferences alone-all aspects of the environment valued in monetary terms?

- Monetary value assigned to species/ecosystems [or saying nothing in life irreplaceable (or has substitutes)?

- No time-specific estimation of benefit

- Either assumes perfect foresight or neglects the uncertainty in environmental damage.

- Assumption of reasonably small changes in the environmental quality. (Johansson 1990).

- Measurement of ‘willingness to pay’- Price information needed(demand) [difficult through market mechanism]

DIFFERENT METHODS OF VALUATION

The methods of valuation may be broadly classified as follows:

- Comparative Sales

- Land and Building

- Income Capitalization

- Profit Capitalization

- Hypothetical Development Scheme and Hypothetical Building Scheme methods.

The sale price of the property, if the sale has occurred on a date proximate to the date on which the valuation is required, and if the sale price data is authentic and reliable, will itself give the market value of the property. This would, thus, give an excellent method for the correct valuation of an immovable property. However, it is rare that such an event occurs and is also reliable, and yet, an independent valuation is required. That is why, though in theory the sale price method could be considered as yet another method for valuation, in actual practice, this hardly has any practical significance.

In general, any method, theoretically at least, should give me, or at least more or less the same value. However, it is invariably either not possible or not practical to adopt all methods in all situations. The success of any method in giving a reasonably correct assessment of value depends on the availability and reliability of basic input parameters required in adoption of the chosen method. Moreover, the properties are invariably fraught with some or the other encumbrances. Some of the methods may not give the facility of conveniently accounting for such encumbrances.

For example, when a property is tenanted, and the tenants are protected against eviction and against enhancement of rents, the Land and Building method does not provide any ready means for accounting for a reduction in value of the property in the hands of the landlord due to the encumbrances of such a tenancy. Also, methods of the Hypothetical Development Scheme and Hypothetical Building Scheme are rather sensitive to variation in basic assumptions and can, at best, be used with caution, and that too if no other method is conveniently applicable.

a) Comparative Sales Method

Comparative Sales method is the ideal method for valuation if reliable data of comparative sales is available. However, it is rare that one comes across the sale instance of a comparable built-up property sold on the date, or even near about the date, on which the value of a property is to be determined. It is, however, usually possible to get reasonably reliable data for comparable plots of land. The method is, as such, the most reliable method for determining the value of land. Even while adopting this method for the valuation of land, it is usually necessary to make adjustments for the differences between the subject property and the chosen comparable sale(s).

b) Land and Building Method

Land and Building method contemplates the determination of the value of land separately, and then adding to it, the value of the structures. The philosophy governing this method is that any prudent buyer may be prepared to pay, and any prudent seller may be prepared to take, that amount as the price of the property, as would be required to build another property which is similar in all respects to the subject property. This method is found to be useful in all normal property valuation cases where there are no apparent restrictions on full enjoyment of the property by the buyer. The method presupposes that the property is to be passed on in a vacant state, or at least, the tenants do not have statutory protection and can be evicted at will. It also presupposes that it is possible to build another property with similar facilities and in a similar locality.

c) Income Capitalization Method

Income Capitalization method is recognized to be the most appropriate method for determining the value of a property which is tenanted and where the tenants enjoy protection under rent control laws against eviction and against enhancement of rents. In such cases the property value virtually gets divided into two parts. One part pertaining to the right of occupation in the hands of the tenant is usually not a legally saleable commodity. The other part relating to the ownership of an encumbered property, including the right to receive rents, remains with the landlord. It is the latter part which is usually required to be valued. And since this part predominantly relates to the right to receive rent, the most favored method is the income capitalization method.

d) Profit Capitalization Method

Profit Capitalization method is also a slightly modified form of the Income Capitalisation method with a little variation. This method is invariably applied to commercial, usually single-use properties used in business ventures. A cinema house, or a hotel, run as a business venture by the owner, generates profit for the owner due to the very nature of the property. It is considered that the property plays a predominant role in the generation of profit in such cases.

Many valuers, therefore, use this method for determining the values of such properties by substituting profit (after making a reasonable reduction to account for the entrepreneur’s effort) in place of income in the Income Capitalization method. The method is found to be quite useful in cases where the comparative land rates data is not available.

e) Hypothetical Development Scheme and Hypothetical Building Scheme Methods

Hypothetical Development Scheme and Hypothetical Building Scheme methods are evolved from a combination of the Land and Building method and the Income Capitalization method. These methods are used when no reliable data for land rates for comparable instances is available, but the data for prevalent rates of small plots of land, or for rents receivable in the locality, can be obtained. The methods may be applied, albeit with caution, when a development scheme or a building scheme is feasible according to the prevailing bylaws and/or demand.

DIFFERENT METHODS OF ENVIRONMENT VALUATION

1 . The market pricing approach

-

- Used if real outputs/inputs increase or decrease.

Examples

- Decrease in timber harvest and/or extraction of minerals due to an increase in wilderness area.

- Increase in fish harvest due to new water pollution control technology.

- Increase in crop yield due to higher air quality standards

2. The Replacement Cost Approach

- Measure the market cost to restore or replace

- Example- Reduction in emissions of acid rain precursors –savings on repairing, restoring and replacing infrastructure.

- Replacement and restoration costs reflect people’s willingness to pay to avoid environmental damage.

3. Hedonic Pricing Approaches-

- Environmental amenities are associated with property values

- Environmental features affect property

Housing sites proximity

- Example 1, with a landfill site

- Example 2: an airport,

- Example 3 vicinity to the nuclear plant

Hedonic Valuation in Practice:

- Statistical methods to estimate the value of facilities due to environmental attributes or amenities.

- Create a functional relationship between independent and dependent variables. (In case of housing, dependent variables market prices; independent variables – location, lot size, scenery, no of rooms, floor space, facilities, age, area, and property tax level, etc).

- Data fitting for developing hedonic price

- Coefficients express the marginal price associated with each attribute.

- Example- effects of a landfill site on a house

Value rises by nearly Rs 5,00,000 for each km away from the landfill (6% per km)

- Valuation of health risks stemming from exposure to workplace environmental hazards

Economic valuation of changes in human health conditions- mortality (premature death) and morbidity (illness) associated with occupation.

Willingness to pay inferred from medical expenditures and differential wages

Pollution – health risk. Eg, groundwater contamination by toxic waste

Ex 2- workplace exposure to toxic chemicals, carcinogens, or other environmental hazards.

- How to monetize increases the mortality and morbidity rates of a community?

Measuring human ‘life’, pain, and suffering? Isn’t life priceless

- Values of ‘life’ or ‘pain’ are not measured, but people’s preferences for health risk – how much damage willing to avoid.

- ‘life’ measurement of ‘statistical life’.

- Assumption: morbidity risks associated with workplace environmental hazards are factored into wages paid by different occupations.

Wage–risk differentials measure changes in morbidity resulting from environmental pollution

4. The household production function

Approach

- Aversive expenditures

- Households’ expenditures on goods and/or services substitute or complement for avoiding environmental damage.

Soundproof walling, water filters, hospital visits, frequent painting of residential dwellings, and so on.

- Households willing to pay to avert specific environmental damage(s).

- So aversive expenditures- a measure of households’

- In many cases, several types of aversive expenditures are undertaken simultaneously. Total benefit by summing the various expenditures

- Travel cost method

- Valuation of environmental services from recreational sites, such as national parks.

- A special technique to estimate the benefit from changes in the environmental amenities of recreational sites.

Measures the benefit (willingness to pay) stemming from a recreational experience, (households’ expenditures on the cost of travel)

5. The Contingent Valuation Method

- Common features of earlier approaches:

- Willingness to pay by using market prices either explicitly or implicitly.

Stress exclusively on estimating use values, benefits or satisfactions of individuals directly utilizing the services (amenities) of natural environment

Valuation questionnaire-

Example: – The Case of the Kalama Zoo Nature Center

Four important issues for a good Contingent valuation survey:

- Include additional questions to capture respondents’ demographic characteristics and socioeconomic

- Include questions to determine the actual motivation of a respondent’s vote.

- If vote an expression of preference or opinion or protest?

- Important since it just captures individual preference and nothing else.

- Identification of the relevant population and the determination of sample size

- Mode of Survey – personal or telephone interviews or mail surveys (or in combination).

- Contingent valuation expensive.

- But capture the use values and non-use values of any type of environmental asset.

- Recent applications. Mixed but encouraging results

Detailed Case Study

Valuation of water resources

Life Cycle Cost Analysis (LCCA)

Life Cycle Cost Analysis (LCCA) is an analytical method that can assist in selecting the most cost-effective water supply alternative that can achieve the desired long-term service life and meet the needs of a community.

LCCA enables a community or project sponsor to compare the total costs, Overtime, of multiple alternatives, each of which may be appropriate for implementation. Under a simpler scenario, if a single alternative is selected, LCCA can be used to better understand the timing of total costs associated with that project–from its beginning stages, to the end of its useful life. LCCA considers general guidelines and best practices for application and follows basic economic principles to encourage uniformity and achieve useful results.

LCCA, in lieu of only calculating initial capital construction costs, is essential in evaluating all of the long-term implications of different strategies to achieve a next-ended service life, but which have different levels and timing of cost requirements.

Generally speaking, key elements in the LCCA include initial costs and all relevant future costs associated with required inspection, maintenance, repair, rehabilitation, and possible component replacement, including associated demolition, disposal, and user costs.

https://youtu.be/XRCXR4aw6Bo?si=IKuK_L6VnaJnl-43