REGISTRATION OF VALUERS UNDER SECTION 34 AB OF WEALTH TAX ACT-1957

ALL YOU NEED TO KNOW ABOUT

Section 34AA of the Act provides that notwithstanding anything contained in this Act, any assessee who is entitled to or required to attend before any wealth-tax authority or the Appellate Tribunal in connection with any matter relating to the valuation of any asset, except where he is required under this Act to attend in person, may attend by a registered valuer.

Qualifications for Registered valuer

Rule 8A of the Wealth Tax Rules, 1957 provides the qualifications of the Registered Valuer. The said Rule prescribes the qualifications for registration of valuers of different classes of assets.

1. Valuer of immovable property

Rule 8A(2) prescribes the qualifications for registered valuer for immovable property, other than agricultural lands, plantations, forests, mines, and quarries as below-

- The Valuer must-

- be a graduate in civil engineering, architecture, or town planning of a recognized university; or

- be a post-graduate in the valuation of real estate from a recognized university; or

- possess a qualification recognized by the Central Government for recruitment to superior services or posts under the Central Government in the field of civil engineering, architecture, or town planning; and

- (A) he must be a person formerly employed-

- in a post under Government as a gazetted officer; or

- in a post under any other employer carrying a remuneration of not less than ₹ 2,000 per month,

and, in either case, must have retired or resigned from such employment after having rendered service for not less than 10 years as a valuer, architect, or town planner, or in the field of construction of buildings, designing of structures, or development of land; or

- as a professor, reader, or lecturer in a university, college or any other institution preparing students for a degree in civil engineering, architecture or town planning, or for any qualification referred to above and must have retired or resigned from such employment after having taught for not less than 10 years any of the subjects of valuation, quantity surveying, building construction, architecture, or town planning;

OR

- (B) he must have been in practice as a consulting engineer, valuer of real estate, surveyor, or architect for a period of not less than ten years ( in case he possesses a post-graduate in the valuation of real estate from a recognized University- two years) and must have acquired experience in any of the following four fields:-

- valuation of buildings and urban lands; or

- quantity surveying in building construction; or

- architectural or structural designing of buildings or town planning; or

- construction of buildings or development of land;

and his gross receipts from such practice should not be less than fifty thousand rupees in any three of the five preceding years. In case if he is possessing post-graduate in the valuation of real estate from a recognized university his gross receipts from such practice should not be less than ₹ 50,000/- in any of the two preceding years.

2. Valuer of agricultural lands

Rule 8A (3) prescribes the qualifications for the valuer of agricultural lands, other than plantations which are as follows-

- he must be a graduate in agricultural science of a recognized university and must have worked as a farm valuer for a period of not less than five years; or

- he must be a person formerly employed in a post under Government as a Collector, Deputy Collector, Settlement Officer, Land Valuation Officer, Superintendent of Land Records, Agricultural Officer, Registrar under the Registration Act, 1908, or any other officer of equivalent rank performing similar functions and must have retired or resigned from such employment after having rendered service in any one or more of the posts aforesaid for an aggregate period of not less than five years.

3. Valuer for plantations

Rule 8A (4) prescribes the qualifications for valuer of plantations, such as coffee plantation, tea plantation, rubber plantation, cardamom plantation which are as follows-

- he must have, for a period of not less than five years, owned, or acted as manager of a coffee, tea, rubber or, as the case may be, cardamom plantation having an area under plantation of not less than four hectares in the case of a cardamom plantation or forty hectares in the case of any other plantation; or

- he must be a person formerly employed in a post under Government as a Collector, Deputy Collector, Settlement Officer, Land Valuation Officer, Superintendent of Land Records, Agricultural Officer, Registrar under the Registration Act, 1908, or any other officer of equivalent rank performing similar functions and must have retired or resigned from such employment after having rendered service in any one or more of the posts aforesaid for an aggregate period of not less than five years, out of which not less than three years must have been in areas, wherein coffee, tea, rubber or, as the case may be, cardamom is extensively grown.

4. Valuer of forests

Rule 8A(5) provides that a valuer of the forest must be a person formerly employed in a post under Government and must have retired or resigned from such employment after having rendered service for not less than five years in a gazetted post requiring specialized knowledge in forestry.

5. Valuer of mines and quarries

Rule 8A (6) provides that a valuer of mines and quarries shall have the following qualifications-

- he must be a graduate in the mining of a recognized university, or must possess a qualification recognized by the Central Government for recruitment to superior services or posts under the Central Government in the field of mining; and

- he must be a person formerly employed-

- in a post under Government as a gazetted officer, or

- in a post under any other employer carrying a remuneration of not less than ₹ 2,000 per month,

and, in either case, must have retired or resigned from such employment after having rendered service as a mining engineer for not less than 10 years.

6. Valuer of stocks

Rule 8A(7) provides that a valuer of stocks, shares, debentures, securities, shares in partnership firms and of business assets, including goodwill but excluding those referred to in sub-rules (2) to (6) and (8) to (11), shall have the following qualifications, namely-

(i) he must be a member of the Institute of Chartered Accountants of India or the Institute of Cost and Works Accountants of India or the Institute of Company Secretaries of India; and

(ii) (A) he must have been in practice as a chartered accountant or a cost and works accountant or a company secretary for a period of not less than ten years and his gross receipts from such practice should not be less than fifty thousand rupees in any three of the five preceding years, or

(B) he must be a person formerly employed-

- in a post under Government as a gazetted officer, or

- in a post under any other employer carrying a remuneration of not less than ₹ 2,000 per month,

and, in either case, must have retired or resigned from such employment after having rendered service for a period of not less than ten years in the field of audit and accounts or taxation work, or

- as a Company Secretary or a Deputy Company Secretary or an Assistant Company Secretary in a post carrying a remuneration of not less than ₹ 2,000 per month and must have retired or resigned from such employment after having rendered service for a period of not less than ten years.

7. Valuer of plant and machinery

Rule 8A (8) provides that a valuer of machinery and plant shall have the following qualifications-

- he must-

- be a graduate in mechanical or electrical engineering of a recognized university; or

- possess a post-graduate degree in the valuation of machinery and plant from a recognized university; or

- possess a post-graduate degree in the valuation of machinery and plant from a recognized university; or

- (A) he must be a person formerly employed-

- in a post under Government as a gazetted officer; or

- in a post under any other employer carrying a remuneration of not less than ₹ 2,000 per month,

and, in either case, must have retired or resigned from such employment after having rendered service as a mechanical or electrical engineer or valuer of machinery and plant for a period of not less than ten years, or

- as a professor, reader, or lecturer in a university, college or institution preparing students for a degree in mechanical or electrical engineering or for any qualification referred to above, and must have retired or resigned from such employment after having taught for a period of not less than ten years; or

- (B) he must be in practice as a consulting engineer or valuer of machinery and plant for a period of not less than 10 years (in case of a person having post graduate – 2 years) and must have acquired experience in the valuation of machinery and plant and his gross receipts from such practice should not be less than ₹ 50,000/- in any three of five preceding years (in case of a person having post graduate – ₹ 50,000/-in any one of the two preceding years);

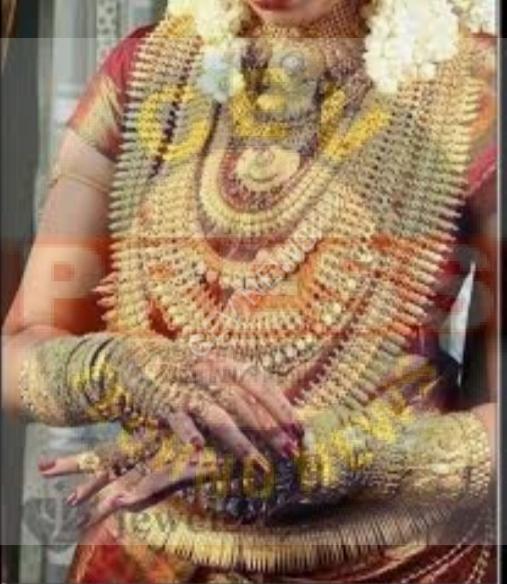

8. Valuer of jewelry

Rule 8A (9) provides that a valuer of jewelry must have been, for a period of not less than five years, a sole proprietor or partner in a partnership firm carrying on jewelry business which has on average an annual turnover of not less than rupees 15 lakhs or profit (including fees for valuation of not less than rupees fifty thousand) in the last three accounting years immediately preceding the year in which the application for registration as a valuer is made by him.

9. Valuer of works of art

Rule 8A (10) provides that a valuer of works of art shall have the following qualifications, namely:-

- he must have specialized by virtue of his academic and professional pursuits in the particular line of art, for the works of which he seeks to be registered as a valuer, and

- he must have served in any one or more of the following capacities, namely:-

- Director-General or Superintending Archaeologist of the Archaeological Survey of India;

- Director of National Museum, New Delhi, Salar Jung Museum, Hyderabad, Prince of Wales Museum, Bombay, Indian Museum, Calcutta, Asutosh Museum, Calcutta, Madras Museum, Madras or Bharat Kala Bhavan, Varanasi;

- principal of a Government School of Art;

- member of the Art Purchase Committee of any of the museums or of the Lalit Kala Akademi.

10. Valuer of life interest, reversions, and interest in expectancy

Rule 8A (11) provides that a valuer of life interest, reversions, and interest in expectancy shall have the following qualifications, namely:-

- he must be a graduate of a recognized university; and

- he must have-

- been in practice as an actuary under the Insurance Act, 1938 (4 of 1938), for a period of not less than ten years; or

- he must have rendered continuous service for a period of not less than ten years as an actuary under the Government or in the Life Insurance Corporation of India established under the Life Insurance Corporation Act, 1956; or

- he must have practiced as an actuary or served as such under the Government or in the Life Insurance Corporation of India for an aggregate period of not less than ten years.

Disqualifications

The following are the disqualifications meant for the registration of a valuer under the provisions of the Act and the Rules-

- No person shall qualify for registration as a valuer, other than as a valuer of works of art if he is employed under the Government or any other employer.

- he has been dismissed or removed from Government service; or

- he has been convicted of an offense connected with any proceeding under-

- the Income-tax Act, 1961 (43 of 1961); or

- the Wealth-tax Act, 1957 (27 of 1957), or

- the Gift-tax Act, 1958, or

- a penalty has been imposed on him-

- under clause (iii) of sub-section (1) of section 271or clause (i) of section 273 of the Income-tax Act, 1961, or

- under clause (iii) of sub-section (1) of section 18of the Wealth-tax Act, 1957, or

- under clause (iii) of sub-section (1) of section 17 of the Gift-tax Act, 1958; or

- he is an undischarged insolvent; or

- he has been convicted of any offense and sentenced to a term of imprisonment; or

- he has been found guilty of misconduct in his professional capacity,-

- in a case where he is a member of any association or institution established in India having as its object the control, supervision, regulation or encouragement of the profession of engineering, architecture, accountancy, or company secretaries or such other profession as the Board may specify in this behalf by notification in the Official Gazette, by such association or institution; or

- in any other case, by the Chief Commissioner or the Director-General in accordance with the procedure laid down in rule 8Fand rules 8H to 8K, which in the opinion of the Chief Commissioner or the Director-General, renders him unfit to be registered as a valuer.

Procedure for registration as a valuer

The following is the procedure for registration of valuer under this Act-

- Any person who possesses the qualifications prescribed on this behalf may apply to the Chief Commissioner or Director-General in Form No. ‘N’ for being registered as a valuer under this section;

- Every application shall be verified in the prescribed manner, shall be accompanied by fees of ₹ 1000;

- The fee will not be refunded if the application for registration is rejected;

- The application shall contain a declaration to the effect that the applicant will-

· make an impartial and true valuation of any asset which he may be required to value;

· furnish a report of such valuation in the prescribed form;

· charge fees at a rate not exceeding the rate or rates prescribed in this behalf;

· not undertake valuation of any asset in which he has a direct or indirect interest.

The Chief Commissioner or Director-General shall maintain a register to be called the Register of Valuers in which shall be entered the names and addresses of persons registered under sub-section (2) as valuers.

Restrictions on practice

Section 34AC of the Act provides that No person, either alone, or in partnership with any other person, shall practice, describe himself or hold himself out as a registered valuer for the purposes of this Act or permit himself to be so described or held out unless he is registered as a valuer or, as the case may be unless he and all his partners are so registered under this Chapter.

No company or other body corporate shall practice, describe itself or hold itself out as registered valuers for the purposes of this Act or permit itself to be so described or held out.

Furnishing of information

Section 34ACC of the Act provides that Where any person who is registered as a valuer under section 34AB or who has made an application for registration as a valuer under that section is, at any time thereafter,-

- Where any person who is registered as a valuer or who has made an application for registration as a valuer under that section is, at any time thereafter,-

· convicted of any offense and sentenced to a term of imprisonment; or

· in a case where he is a member of any association or institution established in India having as its object the control, supervision, regulation or encouragement of the profession of architecture, accountancy, or company secretaries or such other profession as the Board may specify in this behalf by notification in the Official Gazette, found guilty of misconduct in his professional capacity, by such association or institution,

he shall immediately after such conviction or, as the case may be, finding, intimate the particulars thereof to the Chief Commissioner or Director-General.

Removal and restoration

Section 34AD provides that The Chief Commissioner or Director-General may remove the name of any person from the register of valuers where he is satisfied, after giving that person a reasonable opportunity of being heard and after such further inquiry, if any, as he thinks fit to make,-

- that his name has been entered in the register by error or on account of misrepresentation or suppression of a material fact;

- that he has been convicted of any offense and sentenced to a term of imprisonment or has been guilty of misconduct in his professional capacity which, in the opinion of the Chief Commissioner or Director General, renders him unfit to be kept in the register.

The Chief Commissioner or Director-General may, on application and on sufficient cause being shown, restore to the register the name of any person removed therefrom.

The Chief Commissioner or Director-General shall, once in three years review the performance of all the registered valuers and may remove the name of any person from the Register of Valuers where he is satisfied, after giving that person a reasonable opportunity of being heard and after such further inquiry, if any, as he thinks fit to make, that his performance is such that his name should not remain on the Register of Valuers.

Guilty of misconduct

Rule 8E provides that for the purposes of section 34AD of the Act, a registered valuer shall be deemed to have been guilty of misconduct in his professional capacity if he has been found so guilty,-

- in a case where he is a member of any association or institution established in India having as its object the control, supervision, regulation or encouragement of the profession of engineering, architecture, accountancy, or company secretaries or such other profession as the Board may specify in this behalf by notification in the Official Gazette, by such association or institution; or

- in any other case, by the Chief Commissioner or the Director-General, in accordance with the procedure laid down in rule 8F and rules 8H to 8K.

Charge sheet

Rule 8F provides that Where the Chief Commissioner or the Director-General, on the basis of information in its possession, is of the opinion that any registered valuer, or any other person, not being a person referred to in sub-clause (i) of clause (e) of sub-rule (13) of rule 8A, who has made an application for registration as a valuer under rule 8B, is guilty of professional misconduct in connection with any proceeding under any law for the time being in force, he shall frame definite charges against such person and shall communicate them in writing to him together with a statement of the allegations in support of the charges.

On receipt of the charge sheet and the statement referred to in sub-rule (1), the person shall be required to submit within thirty days of the receipt of the said charge sheet and the statement or, within such further time as the Chief Commissioner or the Director-General may, on an application made by that person allow in this behalf, a written statement of his defense and also to state whether he desires to be heard in person.

Inquiry

The Chief Commissioner or Director-General may himself conduct the inquiry referred to in sub-section (1) or sub-section (3) or appoint an Inquiry Officer not below the rank of a Commissioner to conduct such inquiry, and for the purposes of such inquiry, the Chief Commissioner or Director-General. The Inquiry Officer so appointed shall have the same powers as are vested in a court under the Code of Civil Procedure, 1908, when trying a suit in respect of the following matters, namely:-

- discovery and inspection;

- enforcing the attendance of any person including any officer of a banking company and examining him on oath;

- compelling the production of books of account and other documents;

- issuing commission.

Proceeding before Inquiry Officer

Rule 8H provides that the following procedure is to be followed in the inquiry before the Inquiry Officer-

- On receipt of the written statement of defense, or if no such statement is received within the time specified, the Inquiry Officer shall inquire into such of the charges as are not admitted;

- The Inquiry Officer shall, in the course of the inquiry, consider such documentary evidence and take such oral evidence as may be relevant or material in regard to the charges;

- The person who has made an application for registration as a valuer, or, as the case may be, the registered valuer, shall be entitled to cross-examine the witnesses examined in support of the charges and to give evidence in person;

- If the Inquiry Officer declines to examine any witness on the ground that his evidence is not relevant or material, he shall record his reasons in writing;

- At the conclusion of the inquiry, the Inquiry Officer shall prepare a report of the inquiry, recording his findings on each of the charges together with the reasons therefor.

Change of Inquiry Officer

Rule 8K provides that If a change of an Inquiry Officer becomes necessary in the midst of an inquiry, the Chief Commissioner or the Director-General may appoint any other Inquiry Officer, not below the rank of a Chief Commissioner or Commissioner and the proceedings shall be continued by the succeeding Inquiry Officer from the stage at which they were left by his predecessor.

Order

- The Chief Commissioner or the Director-General shall consider the report of the Inquiry Officer and record his findings on each charge and, where he does not agree with the finding of the Inquiry Officer shall record the reasons for his disagreement.;

- If the Chief Commissioner or the Director-General is satisfied on the basis of his findings on the Inquiry Officer’s report that the registered valuer or, as the case may be, the person who has made an application for registration as a valuer, is guilty of misconduct in connection with any proceeding under any law for the time being in force, he shall pass an order under section 34AD of the Act removing the name of the registered valuer from the register of valuers or, as the case may be, directing that the person shall not be registered as a valuer.

Procedure where no Inquiry Office is appointed

Rule 8J provides that The procedure prescribed in the aforesaid rules shall, mutatis mutandis, apply when the Chief Commissioner or the Director-General himself conducts the inquiry without appointing an Inquiry Officer

Report of valuer

The report of valuation by a registered valuer in respect of any asset specified shall be in the Form specified thereof and shall be verified in the manner indicated in such Form-

- immovable property (other than agricultural lands, plantations, forests, mines, and quarries) – Form No. O-1;

- Agricultural lands (other than coffee, tea, rubber, and cardamom plantations) – Form No. O-2;

- Coffee, tea, rubber or cardamom plantations – Form No. O-3;

- Forests – Form No. O-4;

- Mines and quarries – Form No. O-5;

- Stocks, shares, debentures, securities, shares in partnership, firms, and business assets including goodwill but excluding those referred to in any other item in this para – Form No. O-6;

- Machinery and plant – Form No. O-7;

- Jewelry – Form No. O-8;

- Works of Art – Form No. O-9;

- Life interest, reversions, and interest in expectancy – Form No. O-10.

Fees chargeable by valuer

Where two or more assets are required to be valued by a registered valuer at the instance of an assessee all such assets shall be deemed to constitute, a single asset for the purposes of calculating the fees payable to such, registered valuer. The lees to be charged by a registered valuer for valuation of any asset shall not exceed the amount calculated at the following rates, namely:-

- On the first ₹ 5.00.000 of the asset as valued – 0.5% of the value;

- On the next ₹ 10 lakhs of the asset as valued – 0.2% of the value;

- On the next ₹ 40 lakhs of the asset as valued – 0.1% of the value;

- On the balance of the asset as valued – 0.05% of the value.

Where the amount of fees calculated is less than ₹ 500, the registered valuer may charge ₹ 500 as his fees.

FORM FOR REGISTRATION UNDER SECTION 34 AB

ONE CAN FILL EDITABLE PDF FORM ONLINE THROUGH THE FOLLOWING LINK

COMPILED BY:-

DR RAJWINDER SINGH

GET ALL RELATED NEWS UPDATES IMMEDIATELY BY JOINING THE SOCIAL MEDIA PLATFORMS OF CEV GROP BY CLICKING THE LINK PROVIDED AT THE BOTTOM OF THIS WEBSITE PAGE.

FOR ALL UPDATES IN EMPANELMENTS & OTHER UPDATED

GET ALL RELATED NEWS UPDATES IMMEDIATELY BY JOINING THE SOCIAL MEDIA PLATFORMS OF CEV GROP BY CLICKING THE LINK PROVIDED AT THE BOTTOM

JOIN WHATS GROUP OF CTN JOIN SOCIAL MEDIA PLATFORMS OF CEV INDIA FOR ALL UPDATES RELATED TO THE PROFESSION

JOIN SOCIAL MEDIA PLATFORMS OF CEV INDIA FOR ALL UPDATES RELATED TO THE PROFESSION

FACEBOOK PAGE CEV INDIA, TELEGRAM GROUP, YOUTUBE CHANNEL

|

Disclaimer : |

|

We take all possible care for accurate & authentic news/empanelment/tender information, however, Users are requested to refer Original source of the Notice / Tender Document published by the Issuing Agency before taking any call regarding this tender. |