There are three primary approaches used when valuing a property, business: cost/asset, income, and market. A valuation expert often considers valuation methods from each approach when arriving at a conclusion of value.

What are the Main Valuation Methods?

When valuing a company as a going concern, there are three main valuation methods used by industry practitioners: (1) DCF analysis, (2) comparable company analysis, and (3) precedent transactions. These are the most common methods of valuation used in investment banking, equity research, private equity, corporate development, mergers & acquisitions (M&A), leveraged buyouts (LBO), and most areas of finance.

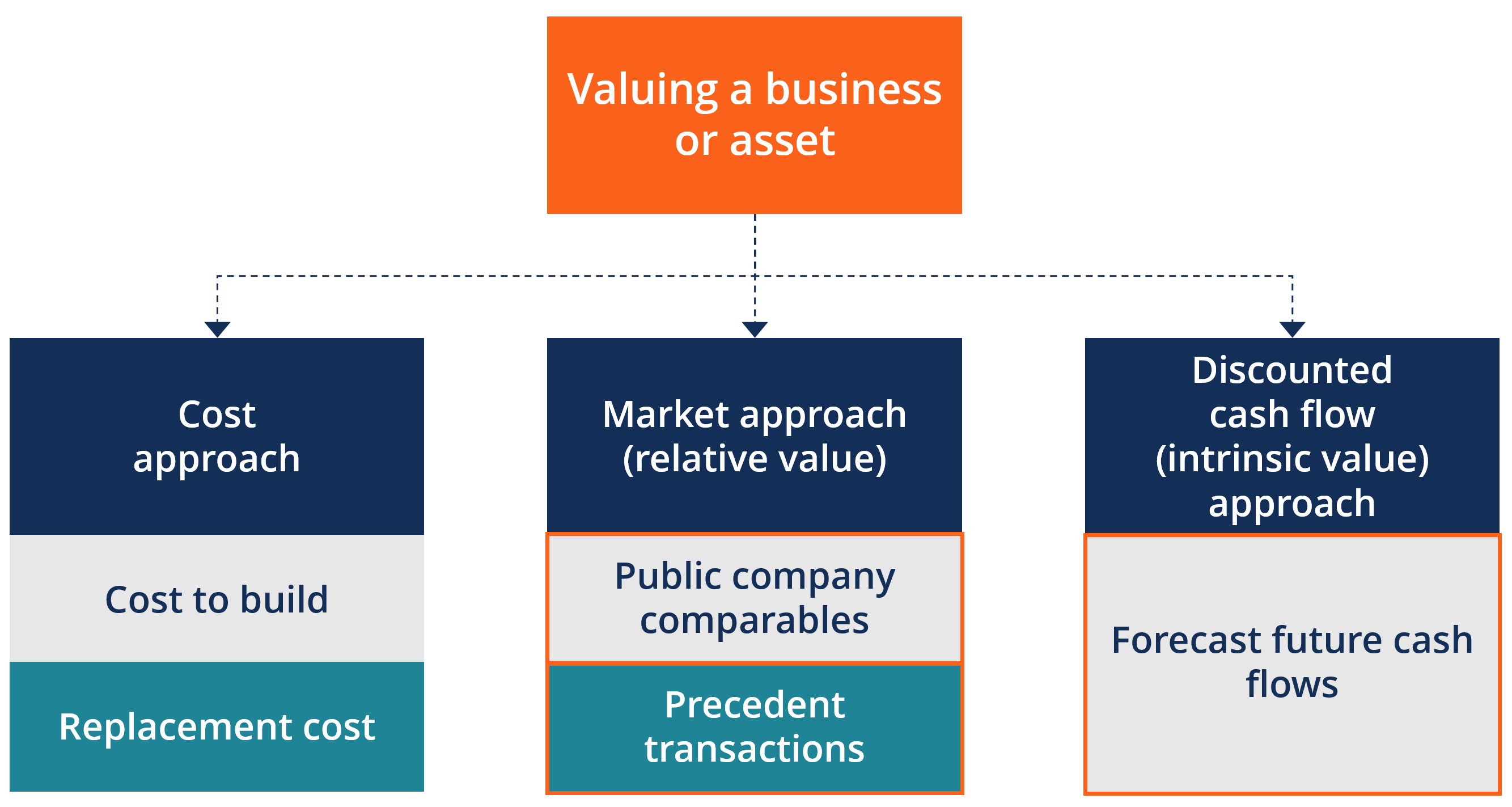

As shown in the diagram above, when valuing a business or asset, there are three different methods or approaches one can use. The Cost Approach looks at what it costs to rebuild or replace an asset. The cost approach method is useful in valuing real estates, such as commercial property, new construction, or special use properties. Finance professionals do not typically use it to value a company that is a going concern.

Next is the Market Approach, which is a form of relative valuation and frequently used in the industry. It includes Comparable Analysis and Precedent Transactions.

Finally, the discounted cash flow (DCF) approach is a form of intrinsic valuation and is the most detailed and thorough approach to valuation modeling. We will describe the methods used in the Market and DCF approaches below.

What is meant by Valuation?

Valuation is the process of estimating the real and market value of a company, a specific instrument, or the value of the business. This term is used in finance to understand the value of an asset. Valuation Approaches are used to estimate the value of the business. These approaches are applied according to internationally adopted principles which are accepted throughout the world. The fair value of a company or an asset is obtained through proper valuation methods. Valuation approaches are derived from the International Financial Reporting Standards (IFRS). According to the standards, as the number of valuation processes increases, valuation professionals would be more in demand.

Use of Valuation Approaches in Business

Valuation approaches are used in everyday business needs. Right from the procedure to sell a company, to transferring a capital instrument from one country to another, to a complex merger and acquisition transaction valuation is extensively used by business and finance professionals. However, the main areas in which valuation is used are as follows:

- Taxation Business– Here, valuation is used to understand the value which is derived in the business post taxation.

- Selling of a company- When the sale of the company is advertised, valuation professionals are recruited to find out the real market or the fair value of the business. Usually, the valuation is done based on a “going concern.” Going concern basis, the valuation is based on the price at which the business assets and liabilities are being sold at.

- Financial Transactions and Financial Planning– Valuation approaches are also used in complex commercial transactions in companies. If a company is planning to raise funds or going for an Initial Public Offering (IPO), then valuation methods have to be adopted. This is also considered in a situation that involves financial planning.

- Foreign Exchange- Transfer of Capital Resources from one country to another– Valuation approaches are also used in a transaction between two different countries, the laws related to foreign exchange would apply. The transfer of capital instruments between the two countries would bring in the provision of valuation. As the prices of capital instruments are subject to fluctuations, proper valuation approaches must be followed by a business.

- Restructuring a business- The business restructuring process also uses valuation. If the activity of the company wants to sell a subsidiary, then to calculate the rate of the subsidiary valuation is used.

- Litigation- Corporate and Civil Litigation would also use valuation processes for understanding the payment/ real value of the assets of the business.

From the above, it is understood that valuation approaches are utilized not only in businesses but are also used for international transactions. However, from the above, it can be understood that the principles of valuation use methods related to finance. These principles of finance develop with the development of business. Therefore there are no specific formulae for a valuation process. Valuation approaches must be prepared according to the particular transaction and the need of the company. Valuation principles have developed due to technical and scientific methodologies.

Valuation Approaches in India

Before the introduction of the Companies Act 2013, there was no specific methodology for carrying out the valuation process. The internationally adopted method for a valuation for the calculation of a capital instrument/ share value of a particular asset was determined based on the Net Assets Valuation method (NAV method). The NAV method has been used exclusively. However, there are various drawbacks of using this method. According to different business valuers, this method of valuation is very restrictive and not right in the valuation approach. Hence there was a requirement of having an independent way of valuation of India. Even the Companies Act 1956, did not bring of a specific method for valuation.

The Companies Act 2013 brought out a specific process when valuation is carried out. One of the steps taken by the Companies Act 2013 was to bring out the system of a ‘registered valuer’. The law relating to the supervision of valuers is under the Companies (Registered Valuers and Valuation) Rules 2017. This regulation explains the meaning of independent valuation that is carried out by a professional agency. It also specifies the procedure of valuation. Apart from this, the organization also monitors valuation agencies throughout the world. A registered valuer is considered as an authority to measure the value of assets and a particular class of assets. Since this was introduced, there was a proper mechanism followed for carrying out valuation processes.

Apart from the Companies Act 2013, the procedures and principles carried out for valuation are monitored and developed by the Securities Exchange Board of India (SEBI). Many transactions would require a valuation, which is carried out by a SEBI registered merchant banker or a Chartered Accountant as per the rules laid down by the Institute of Chartered Accountant of India or a Certified Cost Accountant.

According to the Foreign Exchange Management Act, 1999 (FEMA), the valuation of the transfer of an instrument from one country to another shall be carried out by a SEBI registered Merchant Banker or Chartered Accountant / Cost Accountant. When this form of valuation is carried out, it is done according to international standards adopted by the IFRS.

From the above, it is understood that before the implementation of the Companies Act 2013, the internationally accepted method of valuation was used. However, the NAV method was extensively used in various valuation processes. This was considered to be restrictive to the needs of the business. Therefore with the introduction of the Companies Act 2013, there is specific guidance regarding the generally accepted method of valuation.

Types of Valuation Approaches- Market, Income, and Cost Approach

To come to the right choice of valuation approaches, it is crucial to understand the critical differences between the various approaches to valuation. The international standards of valuation propose three methods of valuation that is used across the globe. The primary valuation approaches used are:

- Market Approach

- Income Approach

- Cost Approach/ Asset-Based Approach

According to the above methods of valuation, there is no right or wrong way, which can be used for valuation. However, simultaneously using all the valuation approaches is not possible. Hence an analysis is required for using the appropriate method according to a specific situation. This will depend on the circumstances of the type of asset or the transaction, which is considered. One method may be suitable for a particular transaction, but the same approach may not be ideal for a transaction involving another form of instrument or asset. Therefore a valuer must analyze the practicalities before considering the valuation approaches.

Valuation Approaches: Which is the best approach for valuation?

There is no universally accepted approach to a proper valuation process. The methodology of valuation must be based on the following factors:

- What is the instrument/ asset/ transaction involved in the valuation process;

- The advantages and disadvantages of choosing the mechanism for valuation;

- The prospects of choosing the method of valuation;

- The approaches that are considered by competitors and other companies in the market; and

- The amount of information which is available regarding a particular method.

Hence valuation approaches are determined not just by a single factor but a combination of multiple factors. To come to the correct method of valuation, the valuer must take into consideration all the above factors. Using various valuation approaches for a particular asset is not allowed. To assess the right approach to valuation, there is a requirement of comparing the real value of all the valuation methodologies to come up with the best method for valuation. If this principle is followed and adopted, then a precise method of valuation can be achieved.

1. Market Approach

MARKET APPROACH

The market approach determines value using similar investments that have been sold in the marketplace. It is defined as:

A general way of estimating a value of an asset, business, or investment by using one or more methods that compare the subject to other assets, businesses, or investments that have been sold or for which price information is available.

There are three common methods used under the market approach: prior transactions of the subject company’s own stock; the guideline public company method; and the transaction (merger and acquisition) method.

All three valuation methods under the market approach usually involve analyzing multiples of revenue or earnings of comparable companies that have been sold. That could involve prior transactions of the company being valued, publicly-traded company multiples, or merger and acquisition transactions that occurred in the marketplace. Experts then apply appropriate multiples to the revenue or earnings of the business being valued.

This is one of the first valuation approaches. This method indicates the requirement of calculating the value of an asset by comparing the asset with similar assets that are present in the marketplace. This can be done with companies also. The products and services offered by companies are compared to businesses providing similar products and services. If there is no proper way to compare the assets of the business to another business, then the valuer has to consider the quantitative and qualitative characteristics of the assets and differences between the asset, which needs to be valued and comparable assets. In other words, this approach can be understood as a comparison method that the company follows to get its assets valued. Publically traded companies are used for comparison in this form of valuation. The market Approach method has the following ways:

- Comparable Transactions Method (CTM)-

From the name of the above method, the valuation is carried out by understanding the similar form of transactions that are carried out in the industry. An example of this form of method is got from the value that is derived from the multiples of revenue or the enterprise value

- Guideline Publically Tradable Comparable Method-

In this method, the asset required to be valued will use other publically traded companies as a guideline to come to an absolute value. The Guideline Publically Tradable Comparable method can only be used as a valuation method when the subject matter or the asset valued is similar to that of the public traded companies. If there are no same types of companies that are dealing with the products or assets which have to be valued, then this form of valuation must not be carried out.

- Guideline for Merged / Acquired Company Method-

In this form of the method, the multiples of transactions of companies in similar industries must be considered and applied to the income of the company.

From the market approach valuation, the methodologies of the market can be understood. Through this method of valuation, the market can be analyzed based on comparison with other companies.

2. Income Approach

INCOME APPROACH

The income approach is often the primary approach for valuing operating companies. It is defined as:

A general way of determining a value indication of an asset, business, or investment using one or more methods that convert expected economic benefits into a single amount. The two primary ways of converting economic benefits into a value indication are the discounted cash flow method (DCF) and the capitalized cash flow method (CCF).

DCF method

DCF is a multiple period valuation models that converts a series of benefit (cash flow) streams into value by discounting them to present value. Experts use a rate of return that reflects the inherent risks in the benefits stream.

CCF method

CCF is a single-period valuation model that converts a benefits stream into value by dividing the benefit stream by a rate of return that is adjusted for growth. This method is a simplified version of the DCF method and is typically used when a valuation expert expects long-term stable cash flows into perpetuity.

This approach uses the principles of economics. There is a formula for this form of approach. The method indicates that the business value is equal to the current value of the income that is generated by the company. Therefore:

Income Approach Formulae: Company Business Value = Income Generated by the company

In this form of approach, the previous earning of the business and the potential earning of the business are taken into consideration. Income-based approaches can be divided into the following:

- Excess Income Capitalisation Method- This method is also called as the Internal Revenue Service (IRS) Method. This can be understood as the business value is equal to the sum of the assets of the business, plus the intangible properties of the business. There is a mixture of two methods here, the income method and the asset method. The valuation of the company is derived from the book value of the potential earning capacity of the company.

- Economic Income Capitalized Method- In this method, the previous earning of the business is taken into picture for valuation. It works on the principle that the earlier revenues of the company are meant to continue as the future income of the business. In this method, the revenues of the business are estimated to be stable based on the historical earnings.

- Discounted Cash Flow Method (DCF Method) – This form of valuation takes into account the valuation based on the future cash flows of the business. This value is determined by considering what returns would be received in the future based on the present amount of investment. The value of the future cash flows of the business is discounted based on the current value of risk based on the amount of investment. This form of valuation is typically used in complex mergers and acquisitions, share sales. This type of valuation is considered when businesses identify that they will grow at a significant basis in the future. This method is one of the signs used methods under the income-based approach of valuation approach.

The DCF method is done by discounting the future cash flows to the present date of valuation. The price of the assets is finalized based on this form of method.

Some factors which are crucial in the discounted cash flow model:

- Present value of the business;

- Future amount of cash flows in the business;

- Finding a method to understand the cash flow process in a business;

- Considering the discount rate regarding the cash flows; and

- Type of asset that is discussed in the business.

3. Cost Approach

COST / ASSET APPROACH

The asset approach, sometimes called a cost approach, is defined as:

A general way of determining a value indication of a business, business ownership interest, or security using one or more methods. It is based on a summation of the value of the assets net of liabilities, where each of the assets and liabilities have been valued using either the market, income, or cost approach.

The asset approach is based on the principle of substitution, where a prudent investor would not pay more for an income-producing property than it would cost them to build or purchase a similar property. This approach derives the value of a business by estimating the value of each of the business’ underlying assets (including tangible and intangible assets) and liabilities.

This approach is most appropriate for valuing real estate, investment holding companies, or capital-intensive companies, such as construction companies with a large amount of equipment.

Of the valuation approaches, the one type of valuation approach is the Cost Approach. This approach mainly focuses on the assets that are present with the business. The focus of this approach is based on the worth of the business and the assets of the business.

Value is obtained by calculating the reproduction value or the replacement cost of assets and subtracting this with the deterioration and other damages that occur to the asset.

This approach is based on the factor that the buyer will pay more for the asset. This would be more economical to consider rather than the cost of purchasing an asset of the same utility. The following approaches are present under the cost approach:

- Net Asset Value Method– This is one of the main methods which are used in business valuation procedures. It is simply calculated as the:

NAV= Value of the Net Assets of the Business- Liabilities of the Business.

The NAV method is extensively used in business dealings.

- Adjusted Book Value Method- The assets and liabilities of the business are adjusted according to the fair market values of the business. This type of valuation is called as the going concern valuation, and it takes all the present value of the assets and liabilities of the business. During this form of valuation, goodwill is no taken.

- Replacement Cost- As the name indicates, the valuation of cost is determined through the cost of a similar asset, which provides the same features and other functions.

- Reproduction Cost Method- When the asset of similar features and qualities is produced, then this is considered as reproduction. Thus in the reproduction cost method, the valuation is got through by reproducing the asset in the same form as the original asset.

- Summation Method- The value of the asset is obtained in this form of the method, by considering the services which are derived from the components of the assets.

Conclusion

ARRIVING AT A CONCLUSION OF VALUE

To arrive at a conclusion, a valuation expert analyzes the value indications from the methods applied along with quantitative and qualitative factors of the subject business. Valuation experts often base their concluded value on one of the valuation methods and use the other value indications to support their conclusion. In other instances, an expert may weigh various value indications to arrive at a conclusion of value.

An expert must take into account all of the relevant factors of the subject interest, the subject company being valued, and the conditions of the economy and industry in which it operates.

Valuation approaches are used in businesses. These valuation approaches are used in different sectors for assessing the real value of the asset or the share. Valuation approaches have to be according to the recommendations made by the IFRS. Businesses consider valuation principles based on the IFRS standards of valuation. Before the Companies Act 2013, one of the main types of a valuation methods used was the NAV method. The Companies Act 2013 brought out the registered valuers rules to come out with a positive approach regarding valuation processes used in businesses.

Market, Income, and Cost Approach are the three methods of valuation. Based on the above three methods of valuation, the business needs to consider certain factors before choosing an appropriate method. The valuer has to know that one method of valuation cannot be used in all valuation processes.